Self Insured Groups:

Myth vs. Reality

Recent accounts of self insured groups run amok has resulted in some resistance to the idea in certain markets. While no risk-sharing program is without risk, CHSI-managed programs are of the highest quality in design and management, traits conspicuously missing from SIG failures you may have seen in the news. In order to illustrate the gap in quality information regarding SIGs, and address some common concerns directly, we offer the following comparisons:

Myth: All Self insured groups are financially risky.

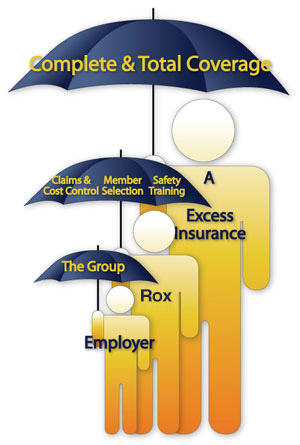

Reality: The risk to employer members of CHSI-managed self insured groups is very low. CHSI-managed self insured groups are well funded with strong financial management. CHSI is SAS 70 audited, ensuring the highest quality of internal controls, and the programs routinely pass regulatory audits. There is risk sharing in self insured groups - members sign an Joint & several indemnity agreement agreeing to share financial responsibility with other members in the event that further funds are needed. The other side of this commitment is that members may receive excess surplus - funds not needed for claims and expenses. Members are protected from additional expenses through a variety of protections: excess insurance, financial audits, detailed financial reporting and board oversight, superior claims performance, expert underwriting, etc.

Myth: If I join a Workers' Comp self insured group and another business in the group has a catastrophic claim - such as a fatality or a paralysis - I will have to pay more money.

Reality: Self insured groups are employer pools - excess losses for one member are ideed absorbed by the rest of the pool. But CHSI-managed self insured groups are fully protected against catastrophic injuries by insurance coverage with 'A' rated excess insurers. The excess carrier covers all costs of all claims that come from a single occurrence, whether it is 1 claim or 100 (such as an earthquake). The group pays an initial amount, normally $500,000, called the Self Insured Retention (SIR). Catastrophic injuries do not in themselves require further funds from group members.

Click below to reveal the reality behind other SIG myths:

Myth: All self insured groups are the same.

Reality: Workers' Compensation self insured groups vary widely. Aside from dramatic differences in state requirements, there are issues of program design and management. In the relatively small number of cases where self insured groups have experienced significant financial difficulty, the program administrator and their operational model have almost always been the primary factor. CHSI is SAS 70 certified. Boards of Trustees receive Fortune 100 quality financials on a monthly basis. CHSI and its managed programs work closely with regulators and have consistently passed state audits without recommendations.

Myth: If another self insured group falters, my group and my business can be forced to pay for their liabilities.

Reality: In the states in which CHSI operates, self insured groups are ultimately supported by the tangible net worth of members. This means that any group needing additional funds must collect the funds from within its own membership. California has additional back-up for self insured employers - the California Self-Insurers' Security Fund - which steps in if any self insured entity cannot meet its obligations.

Myth: If I join a self insured group, I could be responsible for what happens in the group before I join or after I leave.

Reality: Self insured group members only share responsibility for their time of membership. If a member decides to leave the group, their claims liabilities stay with the group, just as they would with an insurance company.

Myth: Self insured groups are unrated and can therefore be a problem for members who need to be with an insurer that has an A.M. Best 'A' rating.

Reality: CHSI-managed self insured groups have met all 'A' paper requirements for members since the first group was formed in 1996. In addition to the 'A' paper of their excess insurance carriers who stand behind the SIG's, the financial and operational controls of the groups and validation of their financial health by state regulators have satisfied all requirements.

Myth: Self insured groups have failed in many states.

Reality: Self insured groups have, in relative terms, had a better track record than insurance companies in terms of continuance of business in states. In cases of self insured group failures, the issue has always been an absence of administrative and underwriting integrity by the program administrator. CHSI maintains strict controls in all of its administrative processes, works closely with its actuaries on maintaining rating integrity and has routinely passed its state audits without recommendations for corrections. CHSI supports licensing for administrators and strong regulatory oversight.